Recap

Anchor Protocol just crossed its 6-month mark since launch on 18 March 2021, and recently marked a phenomenal $4,000,000,000 in TVL. For comparison, the only two lending protocols with higher TVLs than Anchor are Aave ($14b) and Compound ($11b). Aave and Compound have been around for several years and are deployed cross-chain, so it’s a huge feat that Anchor is slowly creeping up to these blue-chip players!

To recap, Anchor is a Terra-native savings protocol offering 18–20% yields on stablecoins. To the TradFi professional or layman, anything above 3% sounds like a dream (or scam). So how is that Anchor is able to provide such high yields? And is that sustainable? You can refer to my research piece here, where I discussed Anchor’s sustainability based on forecasts backed by historical growth rates.

In this article, we look at some statistics over the past 6 months, with a focus on Anchor’s reliance on liquid staking derivatives.

Deposits

The provision of 18–20% yields on stablecoins continues to be attractive as more people enter the crypto space and fall down the Terra rabbit hole. This is particularly noticeable when comparing the growth of Anchor’s deposits against UST’s market capitalisation.

As expected, Anchor’s deposits grew with UST’s market cap. As more people enter the Terra ecosystem, it is natural that their first interaction with a protocol would be to deposit on Anchor for low-volatile stablecoin yields. Buy UST (thereby increasing UST’s market cap), deposit on Anchor (thereby increasing Anchor’s total deposits).

In Anchor’s first month of launch, deposits were 10% of UST’s market cap. As Anchor gained more traction and grew its marketing (you know how outspoken us LUNA-tics can be), Anchor’s deposits as a percentage of UST’s market cap grew as well. In the latest month, the percentage captured seems to have stabilised at 56%.

How can this be used to check against historical growth rates?

I had gotten some great feedback from my previous research piece, and one suggestion was to project Anchor’s growth in deposits as a % of UST’s market cap instead of using historical growth rates. See below.

Historically, Anchor’s deposits have grown by a Compound Weekly Growth Rate (CWGR) of 13.6%. Assuming a 13% week-on-week growth until end of the year (15 weeks), this would result in $9.2b in deposits. That’s unlikely to be the case, since the target for UST’s market cap by end-2021 is $10b and it would be difficult to imagine the entire supply of UST being locked in Anchor.

Let’s assume instead that UST’s market cap grows to $8b by end-2021. We can also assume that Anchor’s deposits continue to absorb 50% of UST’s market cap (marked down from 56% as more protocols are due to launch after Col-5 and that will compete for UST’s market share). That means that by end-2021, there could be $4b of deposits locked in Anchor, resulting in a more realistic 7.4% weekly growth rate from today. The table below shows a sensitivity of the weekly growth rate based on UST’s year-end market cap and estimated % captured by Anchor.

Collateral

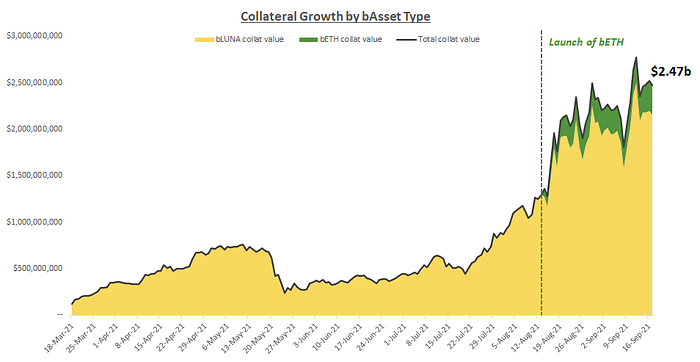

Anchor’s ability to pay depositors a high yield revolves around the provision of liquid staking derivatives (bAssets collateral) to the system. People must be willing to provide bAsset collateral to Anchor, so that Anchor can accrue those staking rewards to fund or subsidise the 18–20% deposit yield. Let’s take a look at how collateral value has grown over the past 6 months.

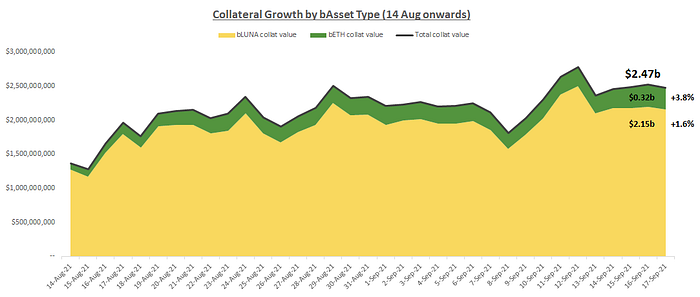

Collateral value has grown at a 12.5% CWGR to $2.47b to date, which is almost on par with Anchor’s deposits growth rate. bLUNA was the only form of collateral until 14 Aug 2021, when bETH went live as the second form of collateral. The below chart shows a closer timeframe from when bETH was launched.

The value of bETH collateral is growing at twice the rate of bLUNA — from $88m to $320m in just over a month (or ~3.8% daily). In the same timespan, bLUNA grew from $1,272m to $2,154m (or ~1.6% daily). This is not surprising, since bLUNA had been growing rapidly for 5 months leading up to this date, and bETH is starting from a lower nominal base.

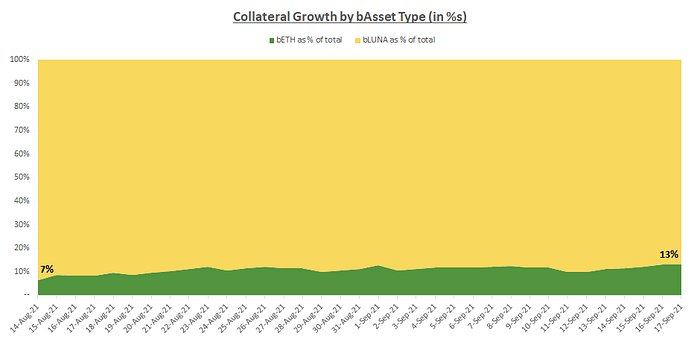

Anchor’s reliance on different collateral types

There are disadvantages to only having one type of bAsset as collateral. In the past, when bLUNA was the only form of collateral, any sudden downswing in LUNA’s price would drastically affect Anchor’s collateral value. This would result in cascading liquidations, which may be detrimental for users and the protocol in a prolonged bear market.

However, the introduction of bETH reduces the risk of price exposure to a single asset, which reduces the likelihood of cascading liquidations. The stacked area chart below shows the % splits of Anchor’s collateral value by bAsset type.

When bETH first launched, it only made up 7% of total collateral value ($88.5m bETH staked as a proportion of $1,360m total collateral). Over time, this has grown to 13% of total collateral value ($320m bETH out of $2,473m total) — which is a good outcome for Anchor’s collateral diversification efforts.

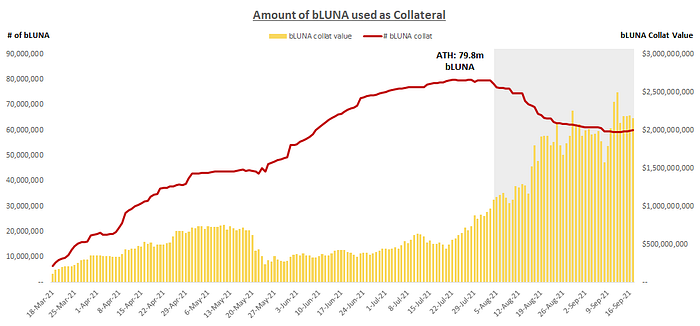

But are users really providing more bAssets as collateral?

Recall that collateral value is a function of two variables: (i) bAsset price and (ii) amount of bAsset supplied to the system.

What if it were the case that collateral value only increased because LUNA’s price was increasing? What if not as many people were providing collateral (number of bLUNAs) to the system than expected?

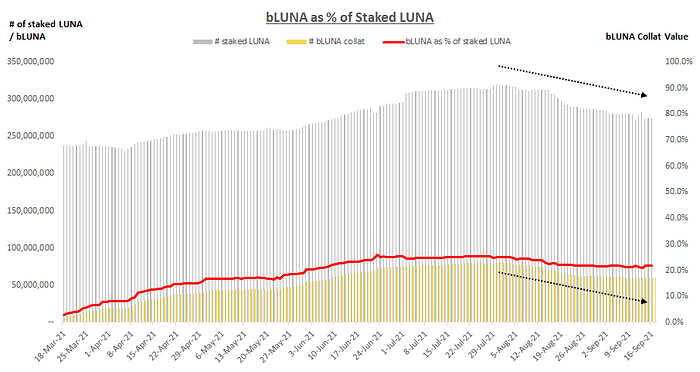

The only way to see this is to isolate the number of bLUNA provided to the system from the impact of the underlying asset’s price. See below.

The amount of bLUNA provided to Anchor had been on a steady increase until end-July (red line). The all-time-high (ATH) was 79.8 million bLUNA supplied as collateral in mid-July. This is commensurate with the market sentiment then — when there was negative sentiment in the June-July period, borrowing incentives were high (distribution APR + low borrowing rate) so many users were willing to provide collateral to Anchor and take out a loan.

In later months (Aug-Sep), bLUNA collateral value was primarily driven by an increase in LUNA’s price, as opposed to more people actually providing bLUNA to the system as collateral. This can be seen in the grey shaded area above, where the number of bLUNA supplied is decreasing (red line) but the collateral value is increasing (yellow bars).

The decreasing amount of bLUNA supplied may be explained by a few reasons:

- Lower borrowing incentives due to the introduction of bETH (dilution of distribution APRs)

- Imminent launch of new protocols (Prism, Levana, etc.) which would give new use cases for LUNA (incentivising users to unbond their bLUNA prior to launch)

- Anticipation of higher staking rewards for LUNA once Columbus-5 goes live (causing users to withdraw and stake on Terra Station instead of providing to Anchor as collateral)

Attempting to validate point 3

If it were true that users were withdrawing bLUNA from Anchor and staking it on Terra Station instead, it should be the case that the supply of staked LUNA is increasing in that same period. Refer to chart below.

In the same period that bLUNA collateral was decreasing (yellow bars), the number of staked LUNA was also decreasing (grey bars). This would invalidate the hypothesis that users were withdrawing bLUNA from Anchor to stake on Terra Station instead. It is therefore more likely that users were generally unbonding bLUNA to prepare for the new use cases of LUNA once new protocols launch.

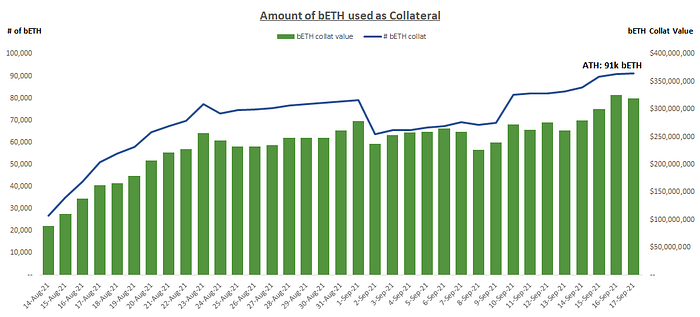

The organic growth of bETH

Going back to the point of collateral diversification, the same approach was applied to bETH to determine whether collateral value is increasing as a result of price or more people providing bETH as collateral.

As shown, the number of bETH being provided as collateral has been steadily increasing since launch. On 14 Aug, 26.8k bETH was provided on Anchor and that figure has grown to 91.3k bETH to date. bETH price has also been range-bound during this period ($3,300–$3,500) so it can be concluded that bETH’s increasing collateral value was a result of more users providing bETH to Anchor as collateral.

A likely explanation is that the net yield received from providing bETH on Anchor and taking out a UST loan, then depositing that UST on Earn results in about 17–20% APY — which is a better yield than most safe ETH farms across the market.

Conclusion

Anchor has been growing at a rapid pace and will likely continue to do so in the coming months. Deposits will continue to grow, albeit at a slower rate than before, as the % share of Anchor deposits as a proportion of total UST market cap reaches a stabilised figure. This should help with prolonging the sustainability of the protocol, although the long-term solution would involve other factors.

Collateral diversification is important to prevent cascading liquidations in a sudden drawdown event and ensure the high deposit yield continues to be adequately funded.

As the Terra ecosystem grows, users will flock to other means of utilising their LUNA or bLUNA, which means fewer being supplied to Anchor as collateral. There is therefore growing importance for Anchor to enable other liquid staking derivatives as an option to subsidise the 18–20% deposit yield (e.g. bSOL which recently went live on Lido).

Other long term solutions could include:

- Finding a way to uncorrelate deposit yields from collateral staking rewards — hinted here by Matt Cantieri, GM of Anchor

- Implementing a dynamic yield mechanism that adjusts according to the value of provided collateral, their associated staking yields and borrowings

This is beyond the scope of this article but will be happy to explore at a later stage!